Course

Introduction to Statistics in Python

4 hr

193K

Optimization is a fundamental tool used across various industries and disciplines to make the best possible decisions within given constraints. Whether it's minimizing costs in a supply chain, maximizing efficiency in energy systems, or finding the optimal parameters in machine learning models, optimization techniques are essential.

Python, known for its simplicity and versatility, offers powerful libraries for optimization problems. Among these, Pyomo stands out as a comprehensive and flexible library that allows users to define and solve complex optimization models seamlessly.

In this tutorial, we will explore Pyomo from the ground up. We'll cover everything from installing and setting up solvers to formulating and solving different optimization problems!

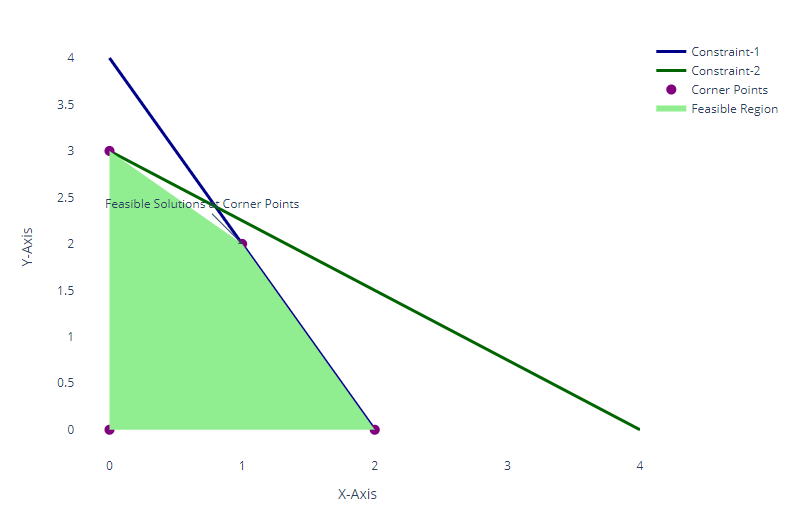

Exploring Feasible Solutions in Linear Programming. Image by Author.

Pyomo is an open-source library for building and solving optimization models using Python. It allows you to define optimization models in a way that's both mathematically rigorous and syntactically intuitive for Python programmers. It supports a wide range of problem types, including:

Now that we understand Pyomo better let’s review some of its most important features.

Pyomo's flexibility comes from its ability to model complex relationships using standard Python constructs. It integrates with various open-source and commercial solvers, making it easy to solve many optimization problems.

Pyomo models are built on Python and written using standard Python syntax. This makes the learning curve gentle for those familiar with Python and allows you to use Python's extensive libraries within your models.

Pyomo has a robust user community and comprehensive documentation, which includes examples and tutorials to help users at all levels.

Pyomo has a wide range of real-world applications. Here are some of them:

Supply chain optimization involves improving logistics, managing inventory levels, and creating efficient production schedules.

This may include minimizing transportation costs, optimizing warehouse locations, or balancing supply and demand.

For example, a company might need to meet customer demand across multiple regions while minimizing shipping costs and maintaining stock levels at each distribution center.

In financial modeling, optimization helps to allocate resources, such as capital, to maximize returns while minimizing risk.

This can involve portfolio optimization, where investors balance risk and reward by selecting a combination of assets subject to constraints like budget limits, regulatory requirements, or risk tolerance.

Financial modeling ensures that financial strategies align with long-term goals while mitigating potential risks.

Optimization in energy systems focuses on maximizing power generation, distribution, and consumption efficiency.

This may involve determining the optimal mix of energy sources (e.g., renewable vs. non-renewable) while minimizing fuel costs, meeting emission limits, and adapting to fluctuating demand.

This type of optimization plays a central role in grid management, power plant operations, and reducing environmental impacts.

Optimization is central to many machine learning and data science tasks, such as hyperparameter tuning and feature selection.

In hyperparameter tuning, optimization algorithms help find the best model configuration to improve predictive performance.

Feature selection, another critical task, involves identifying the most important features that contribute to a model's accuracy, helping to reduce complexity and improve efficiency.

Now that the context is set, let’s get hands-on and start applying Pyomo to some example modeling problems!

Learn more about Python with these courses!

Course

Course

Course

blog

Kurtis Pykes

10 min

Tutorial

Kurtis Pykes

Tutorial

Bex Tuychiev

Tutorial

Zoumana Keita

Tutorial

Matthew Przybyla

Tutorial

Derrick Mwiti