Course

Multivariate Probability Distributions in R

4 hr

8.8K

Few concepts are as fundamental and widely applicable in statistics and data science as the Gaussian distribution. Also known as the normal distribution, this mathematical model underpins countless statistical methods and data analysis techniques.

This comprehensive guide unpacks the concept of Gaussian distributions, exploring their properties, applications, and significance in modern data analysis. We'll examine why they're so prevalent in natural phenomena and how they're used in various fields, from finance to manufacturing.

If you're new to statistics or want to brush up on the basics, our Introduction to Statistics course provides an excellent foundation. For those ready to apply these concepts in specific programming languages, our Statistical Thinking in Python (Part 1) and Statistics Fundamentals with R courses will help you appreciate the many ways in which the Gaussian distribution appears in descriptive and inferential statistics.

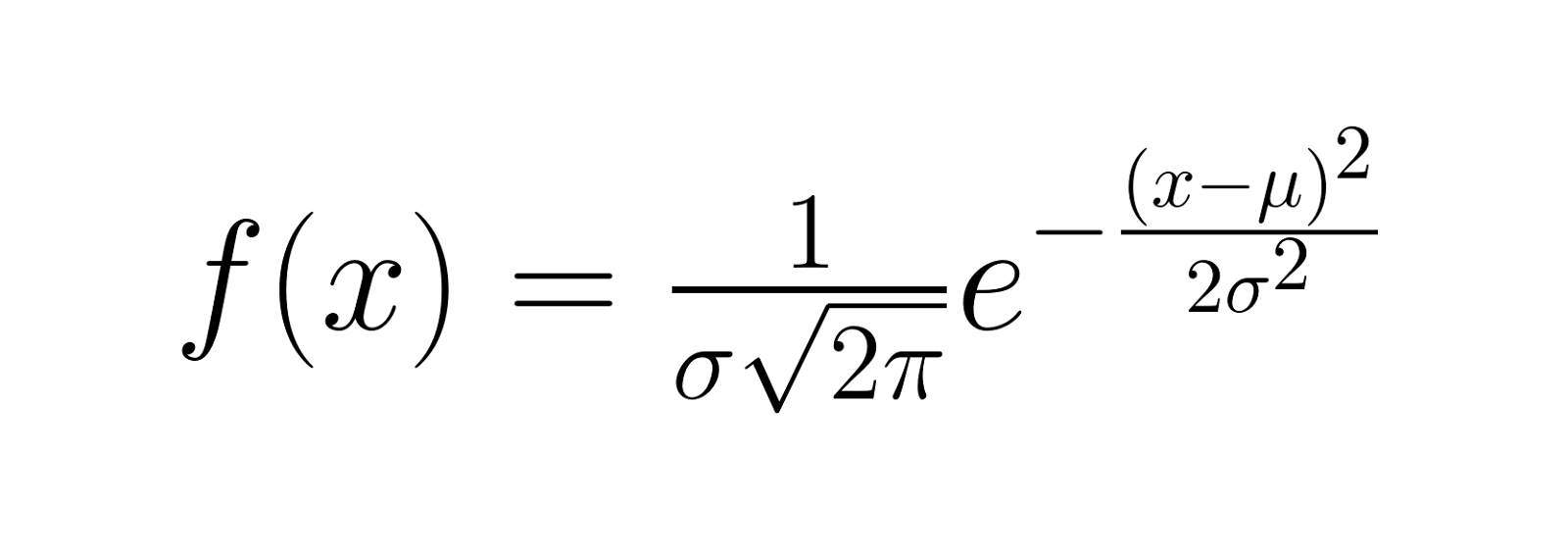

A Gaussian distribution, also known as a normal distribution, is a continuous probability distribution characterized by its bell-shaped curve. It is defined by two parameters:

The probability density function (PDF) of a Gaussian distribution is given by:

Where:

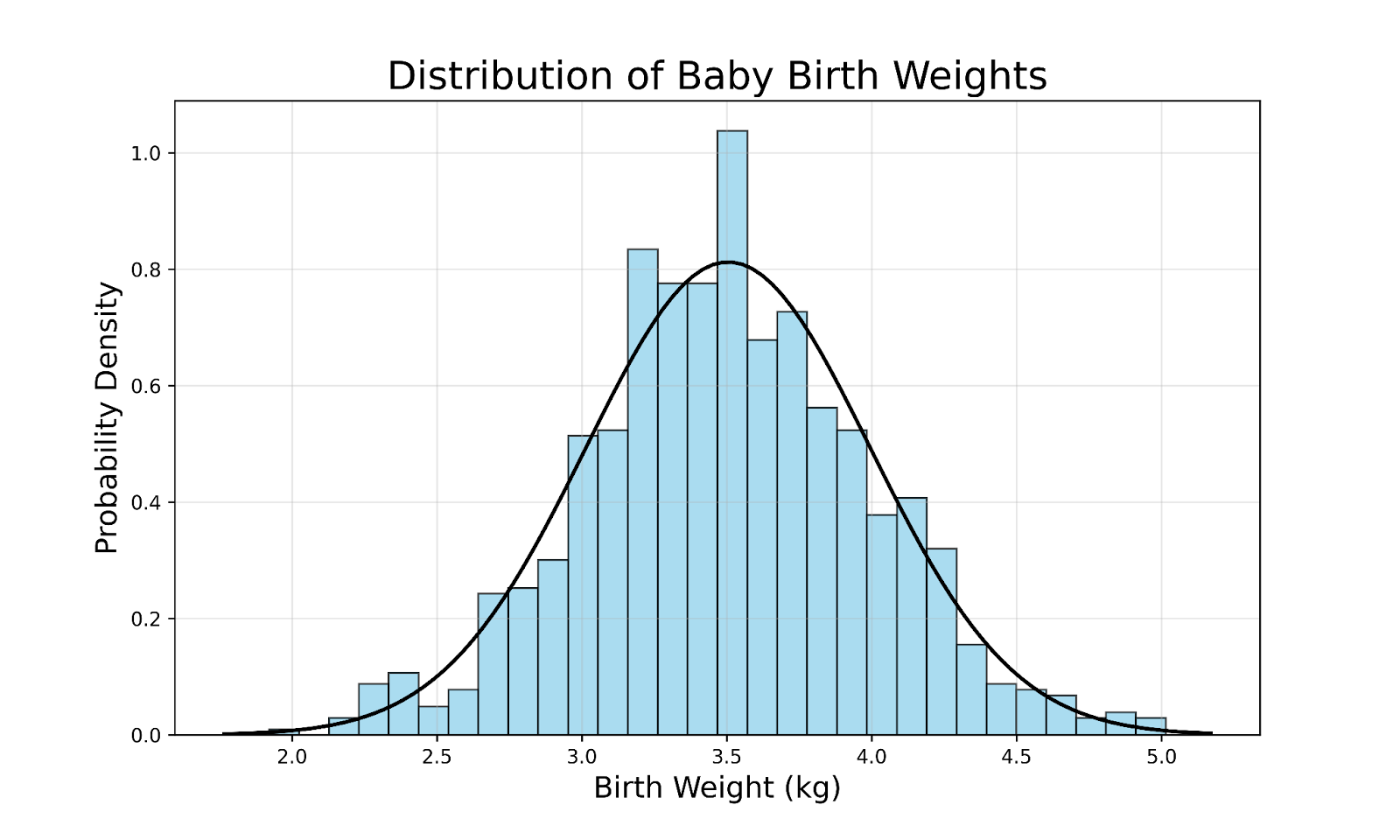

To illustrate the concept of a Gaussian distribution, consider the distribution of birth weights for full-term babies in a large population:

Some key observations from this graph include:

The prevalence of Gaussian distributions in nature and statistics can be explained by the central limit theorem (CLT). The CLT states that the distribution of sample means approaches a normal distribution as the sample size increases (e.g., n ≥ 30) regardless of the underlying population's distribution.

One key aspect of the CLT is that this convergence to a normal distribution happens relatively quickly as the sample size increases. For most practical purposes, even moderately sized samples (e.g., n ≥ 30) are enough for the sample means to approximate a normal distribution. This is true even if the population itself is skewed.

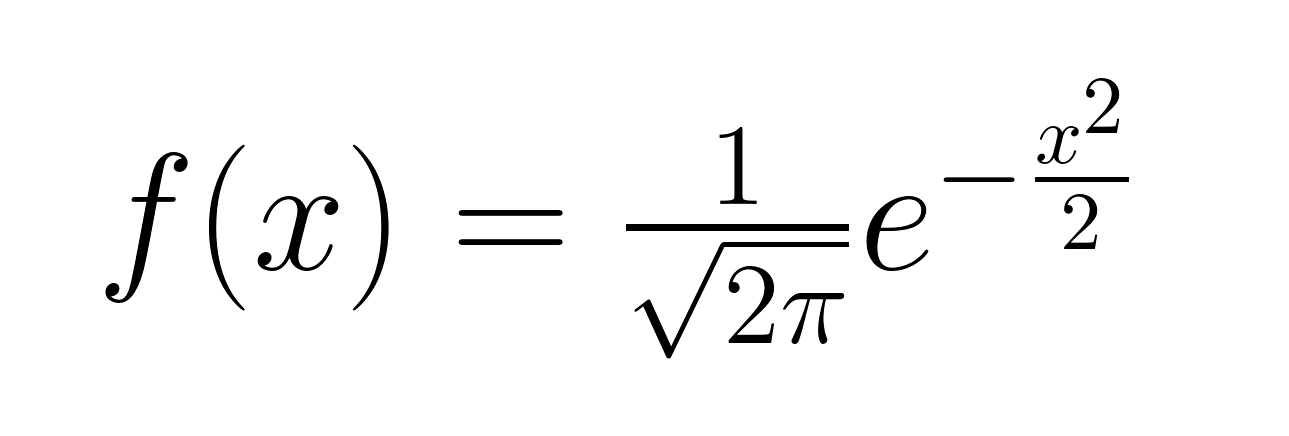

Within the class of Gaussian distributions, there's a special case known as the standard Gaussian distribution, also known more commonly as the standard normal distribution. This is a Gaussian distribution where:

The probability density function of a standard Gaussian distribution is given by the following formula.

Notice that the formula for the standard Gaussian probability density function simplifies from the general form because of the specific values assigned to the mean and standard deviation. Now, let’s visualize the standard Gaussian distribution.

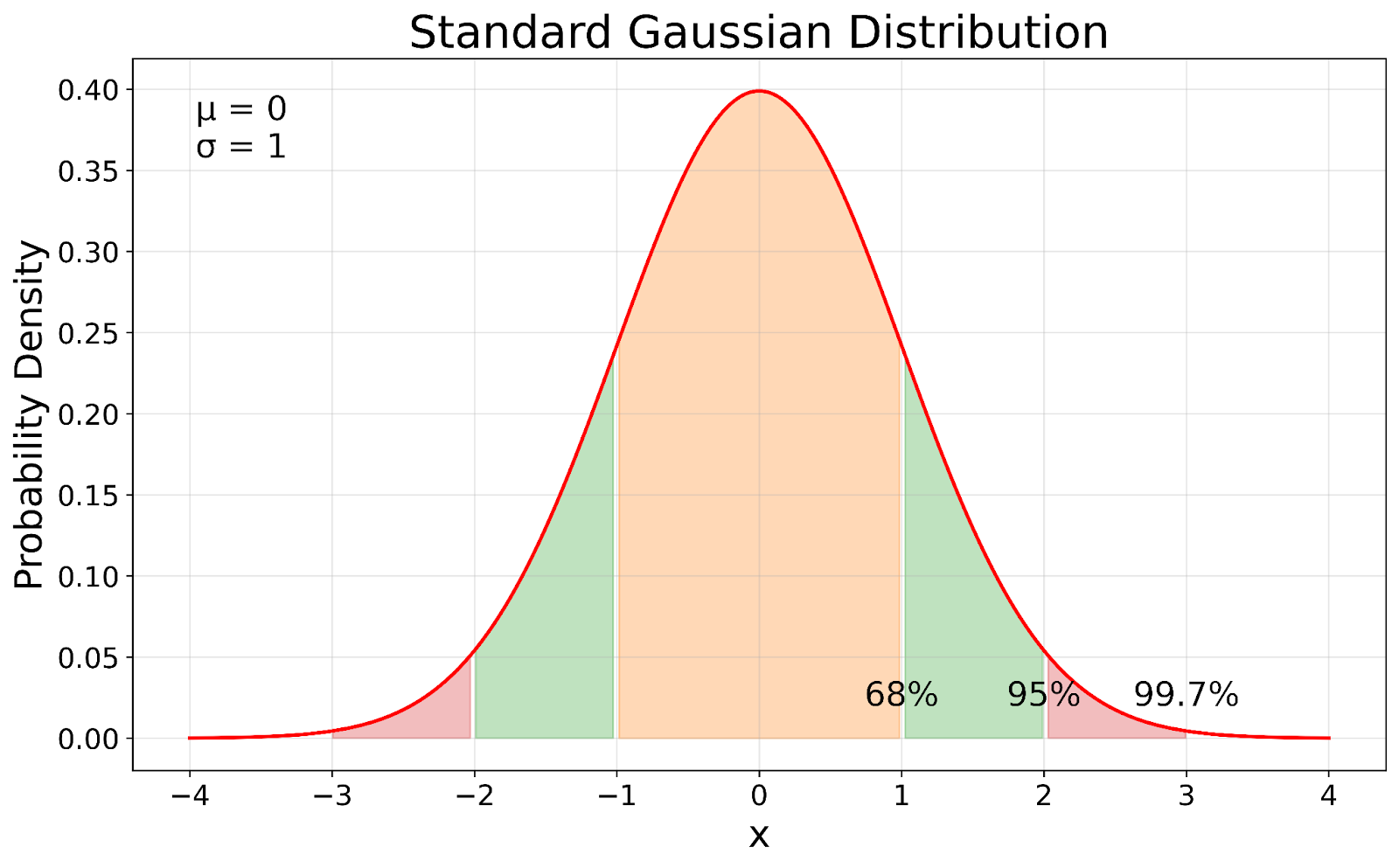

Standard Gaussian distribution. Image by Author

Standard Gaussian distribution. Image by Author

The standard Gaussian distribution, shown in our visualization, serves as a reference point in statistics. In our visual, you can see how the standard Gaussian is a standardized version of any Gaussian distribution. The process of standardization shifts the mean to 0 and scales the standard deviation to 1 while preserving the fundamental properties of the distribution.

Let’s now look at some of the properties of Gaussian distributions.

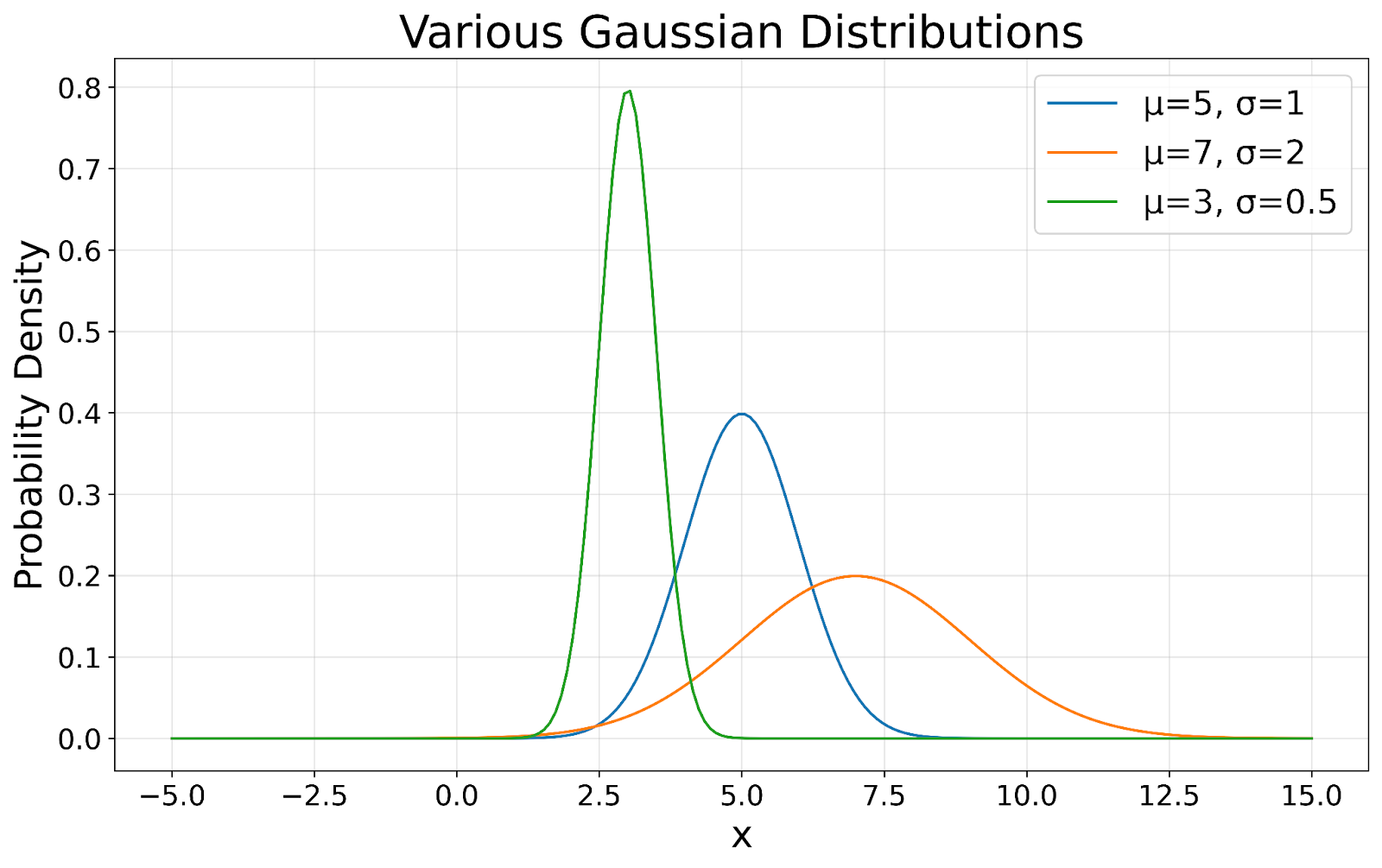

The hallmark of a Gaussian distribution is its symmetrical bell shape. This symmetry means that data is equally likely to fall above or below the mean, which is particularly useful in predicting probabilities and making inferences about data. As shown in the following visualization, all Gaussian distributions maintain this characteristic bell shape, regardless of their mean or standard deviation.

Gaussian distributions visualized. Image by Author

Gaussian distributions visualized. Image by Author

In a perfect Gaussian distribution, the mean (average), median (middle value), and mode (most frequent value) are all the same. This alignment provides a clear indication of the data's central tendency, which is valuable for summarizing datasets. In our visualization, you can see how the peak of each curve represents this central point.

The standard deviation in a Gaussian distribution tells us how spread out the data is from the mean. It follows a predictable pattern:

This rule, known as the 68-95-99.7 rule, applies to all Gaussian distributions, regardless of their mean or standard deviation.

Gaussian distributions are more than just a theoretical concept – they have wide-ranging applications in various fields.

Many statistical tests, such as t-tests and ANOVA, assume that data is normally distributed. These tests help researchers determine if there are significant differences between groups or if observed effects are likely due to chance. The assumption of normality allows researchers to calculate p-values and confidence intervals, providing a framework for drawing conclusions from data and making informed decisions.

The assumption of normality is so important that resampling techniques like bootstrapping have been developed to generate normally distributed resampling distributions from non-normal data, making it easier to construct confidence intervals and perform other statistical analyses. Our tutorial on hypothesis testing showcases how to conduct these tests under various scenarios including situations where data are normally distributed.

Many machine learning techniques rely on assumptions of normality, making Gaussian distributions fundamental to their operation and interpretation. In linear regression, for instance, we typically want to see the y values (dependent variable) follow a normal distribution to have confidence in our estimates. Additionally, we aim for the residuals (the differences between observed and predicted values) to have a normal distribution. These normality assumptions underpin the statistical tests used to assess the model's reliability and the confidence intervals for its predictions.

Also, machine learning scientists might prefer working with data that follows a Gaussian distribution for reasons of computational efficiency. A Gaussian distribution can indirectly contribute to computational efficiency in certain algorithms, especially those that assume or rely on data being normally distributed.

Learn with DataCamp

Course

Course

Course

blog

Josef Waples

10 min

Tutorial

Vinod Chugani

Tutorial

DataCamp Team

Tutorial

Laiba Siddiqui

Tutorial

Vinod Chugani

Tutorial

Vinod Chugani